Duty to Defend

Duty to Defend 2 minute read It is well settled that the duty to defend is greater than the duty to indemnify. But what if the insurance carrier does not have a duty to defend? What are the other alternatives? Most businesses want a duty to defend, and fortunately, that is what most policies use. […]

Operations Limitation

Operations Limitation 2 minute read Does that quote include an Operations Limitation? Maybe it doesn’t sound too ominous. It’s one of those titles on a policy form that is a bit ambiguous. It might apply to an Additional Insured, restricting coverage to the policyholder’s premises, or restricting coverage to a particular project. In fact, limitation […]

Auto Loan/Lease Gap

Auto Loan/Lease Gap 2 minute read Everyone knows the adage that a new car drops in value the moment it’s driven off the lot. Estimates are that the value drops 10-15% immediately, and up to 50% in the first three years. Aside from the economics of purchasing an asset that decreases so quickly, it can […]

Utility Services

Utility Services 2 minute read Consider these loss scenarios: A fire at the electrical utility results in a blackout. The loss of power at a glass factory means all of the glass in process is ruined. In addition, the power shutoff damages several pieces of equipment. A brownout lowers the amount of power coming to […]

Dependent Business Income – Part 2

Dependent Business Income – Part 2 2 minute read ISO uses 5 forms to offer Dependent Business Income coverage. As a reminder, companies which provide this coverage generally have broader terms than ISO uses. Still, it is a good idea to be familiar with basic terms of DBI. The five ISO forms are: Business Income […]

Dependent Business Income

Dependent Business Income 2 minute read Contemplate these loss scenarios: A company manufactures widgets, depending on a main supplier of component parts. The suppliers suspends operations when a truck drives into the building. After current inventory is sold, revenues for the widget manufacturer drop 100%. A farm sells all of its vegetables to a national […]

Educators Legal Liability

Educators Legal Liability, or ELL, is a hybrid of other known policy types. Meant for schools and colleges, it combines the features of management liability policies, such as D&O, EPL and Fiduciary, then adds E&O.

Leasehold Interest

Leasehold Interest 1 minute read Tenants sometimes have favorable building leases, paying less than market rate for the space. For example, in 2008-2010 and again in the COVID era, commercial building owners suffered from low occupancy, and were forced to offer lower rents to attract tenants. Another reason for a low rent might be to […]

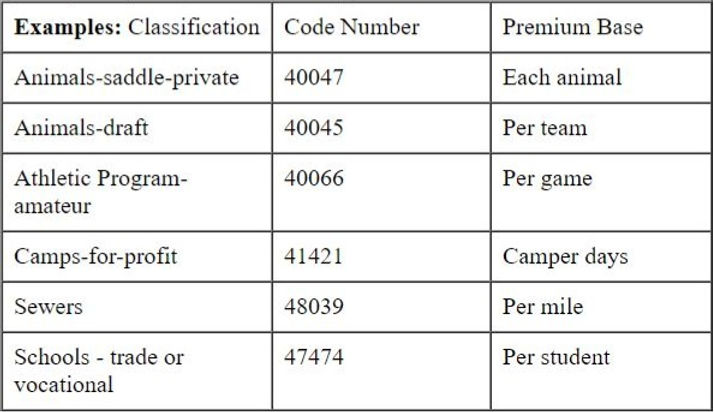

Composite Rating

Composite Rating 1 minute read For policies with 10+ GL classifications, 10+ locations, or 100+ autos, any agent knows the headaches involved with a complex schedule. Getting the schedule right in the first place, tracking changes, and then the audit – these all present challenges. Not only to the agent, but also for the insured […]

Managing Non-Owned Auto Exposure

Managing Non-Owned Auto Exposure 2 minute read Many businesses have non-owned auto exposure, employees driving their own vehicles in the course of business. While the insurance policy may provide coverage, managing the risk is often overlooked. Risk management strategies can be used to reduce this exposure. After a non-owned accident is a bad time to […]

Stand Alone Extra Expense

Stand Alone Extra Expense 2 minute read BusinessIncomeAndExtraExpense. Sometimes we spit out the words so fast, it all sounds like one thing, similar to HiredAndNonOwnedAuto. But in fact, they are separate coverages. Most agents that have a license know that BI can be purchased without EE, but some do not know that EE can also […]

Event Cancellation

Event Cancellation 2 minute read It’s not Event Insurance, it’s Event Cancellation Insurance. With the 2024 Olympic Games running on schedule, take a look back at the 2020 Olympics which were to be held in Tokyo starting in July. In March 2020, the Games were postponed to 2021. This was better news than a total […]

Extended Business Income and Extended Period of Indemnity

Who gives these confusing names, anyway?

Alternatives to Coinsurance for Business Income – Part 2

Does Business Income require coinsurance?

Alternatives to Coinsurance for Business Income – Part 1

Does Business Income for Property require coinsurance?

Business Income for Auto

Does your prospect need BI for their autos?

War Exclusions in Cyber

Is that war exclusion in the cyber policy innocuous?

Voluntary Property Damage

What is Voluntary Property Damage coverage, and who needs it?

Host Liquor Liability

What is Host Liquor Liability, and who needs this coverage?

Dealers Open Lot

Car dealers operate a unique type of business, and need a unique insurance coverage. It is called Dealers Open Lot, or DOL, covering vehicles held for sale by the dealer. These vehicles can be owned by the insured, a lender, or other owner placing the vehicles on contingency sale.

Garage Liability

What is the difference between Garage Liability and Garagekeepers Legal Liability?

Garagekeepers

What is the difference between Garage Liability and Garagekeepers Legal Liability?

Debris Removal

Debris Removal is often an overlooked expense – that is, until after a large loss when the expense may be mostly left to the policy holder.

Specified Causes of Loss

Looking for a way to reduce Auto insurance costs during the hard market? Consider Specified Causes of Loss.

First Named Insured

Does it matter which Insured is listed first?

GL Aggregate Types

Which type of Aggregate Limit does your prospect need?

How GL Aggregates Work

There are so many limits on a General Liability policy, it can be confusing to understand how they interact. This post will give examples of GL claims in action.

VINs

Is a VIN just a serial number? How is it assigned, and does it mean anything?

Vegetation

Is your prospect’s vegetation covered? Does the business owner think it’s covered?

Employment Practices Liability

What is Employment Practices Liability? Is it the same as Employers Benefits Liability? What about Employers Liability?

Employee Benefits Liability

Is Employee Benefits Liability the same as Employers Liability? And if not, then why oh why are the names so similar?

Employers Liability

Employers Liability is the lesser known younger sibling of Workers Compensation. In all but 4 states (see this post), a WC policy has 2 parts: Workers Compensation and Employers Liability. What does EL cover?

Stop Gap

Stop Gap has a specific meaning when it comes to Workers Compensation. Does your insured need it?

Margin Clause

What is a Margin Clause? Can understanding it help win an account? When CP 12 32 is on a policy, the limit is capped at the amount on file in the Statement of Values for a particular property item, plus a stated percentage of that value.

Manufacturers Selling Price

How is finished Stock valued? The additional value of markup or profit margin is not included when the insurer covers a claim.

Punitive Damages

Do your prospect’s liability policies cover punitive damages? Can the answer be used to win the account?

Forgery in a Crime Policy

Does your prospect’s Crime policy cover forgery? Think twice before answering, it’s a trick question.

Cybersecurity and Infrastructure Security Agency (CISA) Services

What’s better than a Cyber policy? Scanning and testing for threats before they happen.

Foundations and Underground Pipes

Does your prospect’s policy cover foundations and underground pipes? Does the business owner think they are covered?

Derivative Lawsuits

What is a Derivative Lawsuit, and how does insurance come into play? With derivative action, the claim is the same (eg, inaccurate disclosures), but the suit is brought on behalf of the company against directors and officers, rather than on behalf of shareholders. It is thought that the company has suffered the harm. Since shareholders believe the company should have taken its own action, shareholders act in the company’s place, or take derivative control for the company. Any settlement is made to the company, rather than to shareholders.

Innkeepers Liability

What is Innkeepers Liability, and does your insured need it? In addition to the need for General Liability coverage, innkeepers need a particular coverage called Innkeepers Legal Liability, informally called Innkeepers Liability.

Guaranty Fund

A Guaranty Fund protects consumers in the case of a failed insurance company. When a policyholder incurs a covered loss under an insolvent carrier’s policy, the loss will be covered by the Guaranty Fund. Just as with All Things Insurance, there are limitations and an exception to the coverage.

Rating Factors in Business Auto

Do you know the 7 features used to rate a business auto risk?

Late Notice of Claim

Can an insurer disclaim coverage due to late notice? The answer is: it depends. Rather than hoping the insured has a defense against late notice prejudice, the best rule of thumb is to always provide timely notice to the insurer.

ERISA

The Employee Retirement Income Security Act, or ERISA, is a federal law that has been amended several times since its passage in 1974. Among other sections, the law says that employers with retirement and welfare benefit plans are required to protect those plans against fraud and dishonesty. The protection is provided through a bond.

Cyber for Restaurants

Change in the restaurant industry is a hallmark of the pandemic. Part of that change includes greatly increased cyber exposure.

Vacant Buildings

Before the pandemic, vacant buildings were less common. Now vacancy is a concern for even class A office buildings, and every main street agent needs to know how to handle it.

Wage and Hour Claims

What is a Wage and Hour Claim, and is it covered by insurance? Understanding this type of claim assists in winning the business, by enabling an agent to point out potential gaps to a prospect.

Seasonal Inventory

When inventory changes seasonally, is there an easier way to manage the BPP limit? Simplifying the process for a prospect and reducing uninsured losses may help win the account.

Hammer Clause

What is a Hammer Clause, and is it beneficial to an insured? Understanding the Hammer Clause enables an agent to point out potential extra expenses to a prospect. Improving this clause can help win the account.

Overinsurance – Property Limits

Save your client some premium and save yourself some headaches and legal troubles. Insure only for replacement cost, plus a possible inflation guard. Your client will likely thank you for insisting on proper limits.

How High Should Liability Limit Be?

Insurance professionals should always offer higher liability limits in writing, whether it is for an Umbrella, Cyber, D&O, Product Liability, the list goes on. The offered limit should be higher than expiring.

Defense Inside – New Nevada Law

Knowledge of the new Nevada law enables an agent to explain coverage differences and premium increases.

Recently Nevada enacted a law prohibiting insurers from issuing or renewing liability policies that use Defense Inside provision. The law takes effect October 1, 2023. Defense Inside is a provision often used in these types of liability policies:

Professional Employment Practices

Cyber Directors and Officers

Product Management

Environmental

Fences

Details on fence coverage enable an agent to point out a gap to a prospect, and to solve the problem in one conversation. Better protection and better pricing is a combination that is hard to beat.

Is your prospect’s fencing covered? For some businesses, that might be a small concern. A 3-foot high cinder block wall between parking lots next to a small restaurant could be negligible. For a manufacturer, an auto dealer, a scrap yard, fencing is a considerable part of the property. Is the fencing covered? Does the business owner think it’s covered?

Both the BOP and CPP forms specifically exclude fences.

Drive Other Car (DOC)

Details on a prospect’s executive auto use can enable an agent to point out a gap, and solve the problem in one conversation. Better protection and better pricing is a combination that is hard to beat.

Are executives and salespeople of your prospect covered when they are not driving for the business? One might imagine the answer, “No! Of course not. We are insuring the business.” But owners, executives, salespeople and others who are provided with a company car perk, use that car for personal use. This could mean such a driver does not have a Personal Auto Policy (PAP).

The Importance of Continuous Learning in the Insurance Industry

The Importance of Continuous Learning in the Insurance Industry 1 minute read In the dynamic and ever-evolving world of insurance, staying ahead of the curve is crucial to success. As insurance professionals, we understand the significance of continuous learning and its impact on our ability to provide exceptional service to clients. In this blog post, […]